Brunswick (BC) – Earnings Preview

In yesterday’s trading session, shares of the recreational boat retailer MarineMax (HZO) rose over 13% after a stellar earnings report:

• EPS of $0.11 vs -$0.02 – Beat

• Revenue of $226.9M vs $187.02M – Beat

• Revenue increased 33% Y/Y

• Same-Store Sales increased 28% Y.Y

• Increased Guidance

• Strong SSS was supported by an increase in larger yacht sales

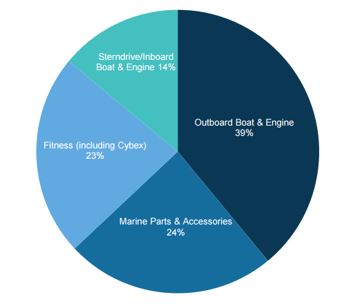

MarineMax’s earning results could be a potentially positive catalyst/read-through for shares of Brunswick (BC), who is set to report earnings tomorrow, January 26th, before the bell. Brunswick is a designer and manufacturer of recreation products worldwide. Below, you will find a quick breakdown of the company’s revenue mix, which shows more than 75% of revenue comes from its Boat/Marine segments:

On January 11th, after Longbow Research conducted channel checks with U.S. dealers, analyst David MacGregor said that U.S. retail sales of Brunswick’s boats appear to have risen 5%-7% last quarter despite a tough comparison. Mr. MacGregor thinks that level of growth would surpass consensus estimates, and he continues to predict that Brunswick’s Q4 EPS will beat the consensus outlook. He kept a $67 price target and a Buy rating on the stock.

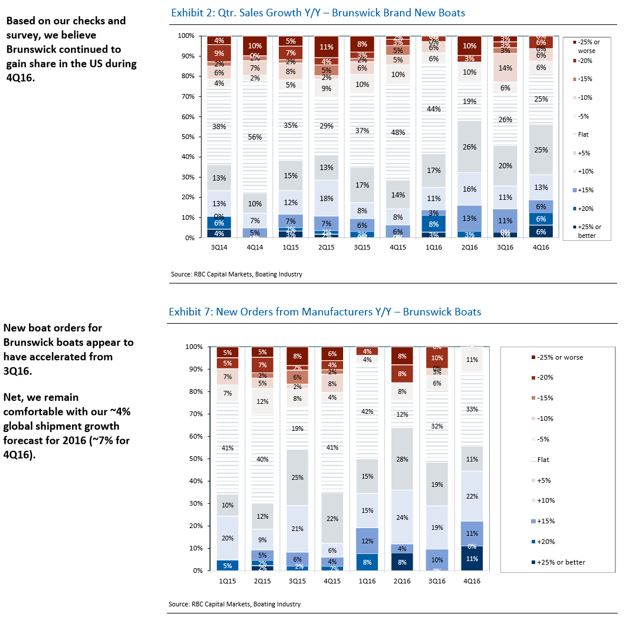

Additionally, RBC Capital conducted its quarterly Boat Dealer Survey and reported its results in its January 20th research note. According to RBC, their survey results and industry checks suggest fairly flat Y/Y (to very slightly down) U.S. retail unit sales in the fourth quarter. They note that Q4 is a seasonally low volume quarter (MarineMax made this same comment on its earnings call), representing ~11% of annual registrations. Preliminary SSI data for October, November, and December support their checks as the three months turned in sales growth of -0.8%, +2.6%, and -2.2% respectively.

In terms of Brunswick, RBC believes the company continued to gain share in the U.S. during Q4 (Figures shown below). More importantly, new boat orders, which drives shipment growth, appears to have accelerated from Q3 (which was +12%). They remain comfortable with their ~4% global shipment growth forecast for 2016 (~7% for Q4), which is against a 2% global shipment comp in 2015. RBC says one thing to watch is BC dealer inventory levels, which do appear to have gotten higher (46% reported inventory are somewhat to high). Bottom-line, RBC says the jump in dealer confidence is encouraging for 2017 and potential decreases in taxes could lead to increased discretionary spending and demand for luxury items. Management will provide 2017 guidance on the Q4 earnings call (and give industry views). They typically guide conservatively, but this backdrop may lead investors to have high confidence in their outlook with the potential for upside.