Ethan Allen (ETH) – Contract Catalysts

As an interior design company, Ethan Allen Interiors is a leading manufacturer, distributor, and retailer of home furnishings and accessories that sells a full range of products through its 300-plus stores worldwide.

On Monday, in the chat room, we highlighted an unusual buyer of 1,050 May 30 Puts for 1.70 on the offer on a wide bid/ask spread of 1.35 x 1.70. This was approximately a $178,000 bearish bet with earnings historically taking place later this month (no confirmed date yet).

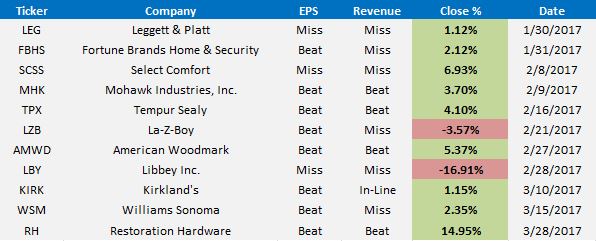

While it’s not apples to apples, it should be noted that while Ethan Allen closed lower by over 12% in its last release (Q2) on January 25th, we’ve been seeing a lot of the Home Furnishing stocks trade higher after reporting their Q4 earnings numbers (snapshot shown below).

Based on the company’s Q2 conference call in late January, contracts, among other things, were one of the main topics of discussion. Before providing the conference call commentary, let me elaborate on the high-profiled contracts Ethan Allen currently has:

State Department – In early August, the company announced it had been awarded a blanket purchase agreement (“BPA”) for the Department of State employees and family residences located abroad. The company said that the BPA is effective for approximately five years, until July 28, 2021. It was also a multiple award schedule, so it is likely that one or more other furniture companies were also awarded a BPA for the Worldwide Residential Furniture Program. The program has a ceiling amount of $300M in total orders, which averages $60 million per year in potential annual order volume under the program that may be subject to bid by the BPA awardees.

Walt Disney (DIS) – In late September, the company announced a partnership where it would launch a collection of Disney-themed furniture and home accessories on November 18th. This collection included things like chairs, ottomans, chests, coasters, pillows, etc.

Amazon (AMZN) – Just announced this week, Ethan Allen will collaborate with Amazon and sell its products through the Amazon website. A slightly smaller SKU set will be available on Amazon than what is available on Ethan Allen’s website. The Amazon offerings will focus primarily on in-stock items (including accent pieces) and the quick ship options (products delivered within 30 days). The logistics of the sales are fairly similar with the company’s existing e-commerce platform, in which all of the interaction with the customer, including delivery, is handled by the retail stores. This partnership is expected to launch this summer. Stifel was out with a note saying, “We’d see this as an opportunity for the company to capture additional customers without much risk or additional spending.”

Moving on to specific conversations within the company’s Q2 conference call:

Bobby Griffin from Raymond James asked “Just real quickly, can you [CEO Farooq Kathwari] or Corey maybe provide an update on the government State Department contract and kind of how the timing of that contract is progressing now that you guys have been awarded part of the bid?”

CEO Farooq Kathwari responded “Bobby, yes we have been but unfortunately the government works very, very slowly. They have still not completed all the information we need but having said this we have started receiving orders. I would think that they have got to give numbering to all these items. We are all ready but they have not completed their numbering.”

Mr. Kathwari went on to say that this is really unfortunate the way they operate, but despite that, they have started to get some orders but he thinks that the orders will really start coming in the fourth quarter of this year.

Jeremy Hamblin from Dougherty said, “Well, it sounds like you are seeing some delays here on the State Department contract versus where you would have thought six months ago. And I think it also sounds like Disney maybe is just, at least a time to see delivered sales on that, a little bit further out than had been planned. So given the increase, the ramp in spending, which calculates to about $2 million a quarter, shouldn’t we just be assuming that this is really pushed out into Q4?”

Mr. Kathwari responded by saying, “It is possible. As I said that, (technical difficulty) in a good, but not tremendously high. So these are something that, one, we could meet, but we have got to take a look at what business we get this month and early next month.”

Moving away from contracts, Brad Thomas from KeyBanc asked, “When I look back over the last four or five years, the company historically does lower revenue in its fiscal third quarter than it does in the second quarter. And the earnings typically clock in about 50% lower than what you do in the second quarter. Any reason that the seasonality would be greatly different?”

Mr. Kathwari responded with, “No, Brad. It will be because, generally, our written orders in the second quarter are generally the lowest because December being a low month. That reflects into the deliveries into the third quarter. So I think the third quarter, from a modeling perspective, will be similar to what we did in the past.”

Wall Street currently has 1 Strong Buy Rating, 1 Buy Rating, and 5 Hold Ratings with a consensus price target of $37. Here are some comments since the company’s last earnings release:

January 25th – Stifel maintained their Hold rating and $34PT and said, “Now with the core product more stable and the Disney collection officially launched, the company can put more weight behind advertising to drive traffic. Digital marketing will be doubled. This will be an interesting test to see if its drives traffic as the promotional effort will be reduced.”

January 26th – Dougherty downgraded the stock to Neutral from Buy following Q2 results. Analyst Jeremy Hamblin changed his views given a lack of visibility on the timing and impact on sales catalysts, including Disney Collection launch and US State Department contract, fewer new product introductions, tough 2H 17 comps, and significant downside risk to consensus FY17 and FY18 estimates.

March 14th – Raymond James analyst Budd Bugatch double upgraded Ethan Allen to Strong Buy from Market Perform saying sales comparisons get easier through 2017 while the retailer’s remerchandising effort is behind it, thereby lowering the clearance markdowns. The analyst has a $36 price target on the shares.