Jabil Inc. (JBL) – Margins, Mobility, and Manufacturing

Jabil is one of the world’s largest electronic manufacturing services and solutions providers that does business with a number of companies, including Apple (AAPL), Cisco Systems (CSCO), Hewlett Packard (HPQ), Keysight Technologies (KEYS), LM Ericsson (ERIC), NetApp (NTAP), Nokia (NOK), SolarEdge Technologies (SEDG), Valeo, and Zebra Technologies (ZBRA).

In yesterday’s trading session, there was a block buyer of 3,500 March 24 Puts for $1.10 on the offer, a $385,000 bearish bet. These have the potential to target the company’s Q2 earnings report, which historically take place in mid-March. But more importantly,the next catalyst for Jabil is the company’s Annual Shareholder Meeting on January 24th.

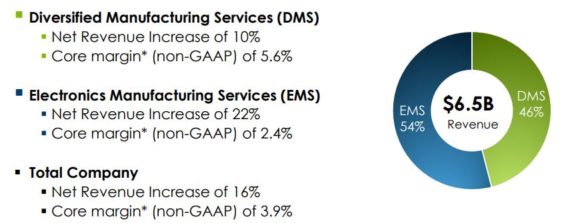

Taking a look at the company’s Q1 earnings report from last month, the company posted decent results with RBC Capital saying the company’s strong EPS print was driven by a combination of better than expected performance in both its Diversified Manufacturing (DMS) and Electronics Manufacturing (EMS) segments with upside driven by new business wins. The company also raised its FY19 revenue guidance by ~$500M to reflect its November quarter beat (~$400M) which suggests ~$100M of revenue upside for the balance of the year. Management continues to see healthcare, packaging, automotive, 5G wireless and cloud contribute meaningfully to its +13% Y/Y revenue growth outlook for FY19.

However, RBC also points out that for the February quarter, while Revenue/EPS guidance came in above consensus, implied operating margin outlook of 3% suggests a 40bps Y/Y decline due to the impact of pre-production costs from new business wins. JPMorgan echoed the same thoughts saying “margins are expanding at a slower pace relative to revenues owing to ramp up cost.”

Apple – BAML was out with a post-earnings note saying that while DMS revenues exceeded guidance by $140mn, the outperformance was driven by healthcare, edge devices, accessories and lifestyle. Mobility was weaker than expected, and remains weak. For now, they are maintaining their iPhone estimates for Dec/Mar quarters at 72mn/48mn, respectively, which are lower than Street estimate of 75mn/50mn, respectively. They would reiterate their Neutral rating on Jabil as risk introduced by high exposure to Apple (~25% of revenues).

CES Recap – Stifel analyst Matthew Sheerin had the opportunity to meet with several executives at Jabil’s CES exhibit, where the company was displaying various products across its end markets, including medical, automotive, industrial, and consumer. Although the session did not generate any incremental news, they did pick up some commentary surrounding tariffs:

• On tariffs, EVP Mike Loparco said Jabil has been working with “many” customers about shifting certain manufacturing out of China, but has actually seen very little movement yet. He added that moving to other low-cost regions in Asia, such as Vietnam, is easier said than done, especially at the scale of Jabil’s customer programs, given the necessary supply chain infrastructure and worker skill sets.